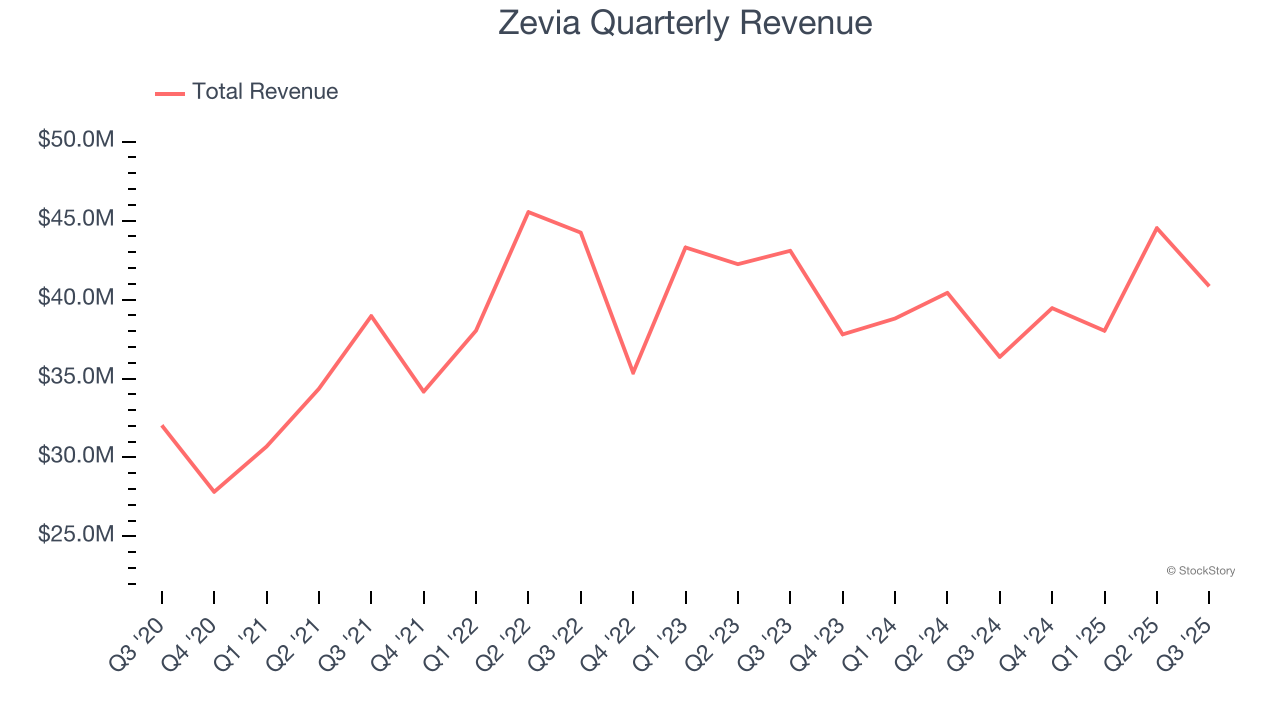

Beverage company Zevia (NYSE:ZVIA) beat Wall Street’s revenue expectations in Q3 CY2025, with sales up 12.3% year on year to $40.84 million. The company expects next quarter’s revenue to be around $40 million, close to analysts’ estimates. Its GAAP loss of $0.04 per share was $0.03 above analysts’ consensus estimates.

Is now the time to buy Zevia? Find out by accessing our full research report, it’s free for active Edge members.

Zevia (ZVIA) Q3 CY2025 Highlights:

- Revenue: $40.84 million vs analyst estimates of $39.39 million (12.3% year-on-year growth, 3.7% beat)

- EPS (GAAP): -$0.04 vs analyst estimates of -$0.07 ($0.03 beat)

- Adjusted EBITDA: -$1.72 million vs analyst estimates of -$3.57 million (-4.2% margin, 51.7% beat)

- Revenue Guidance for Q4 CY2025 is $40 million at the midpoint, roughly in line with what analysts were expecting

- EBITDA guidance for the full year is $5.25 million at the midpoint, above analyst estimates of -$8.8 million

- Operating Margin: -7%, up from -8.2% in the same quarter last year

- Free Cash Flow was -$65,000, down from $3.75 million in the same quarter last year

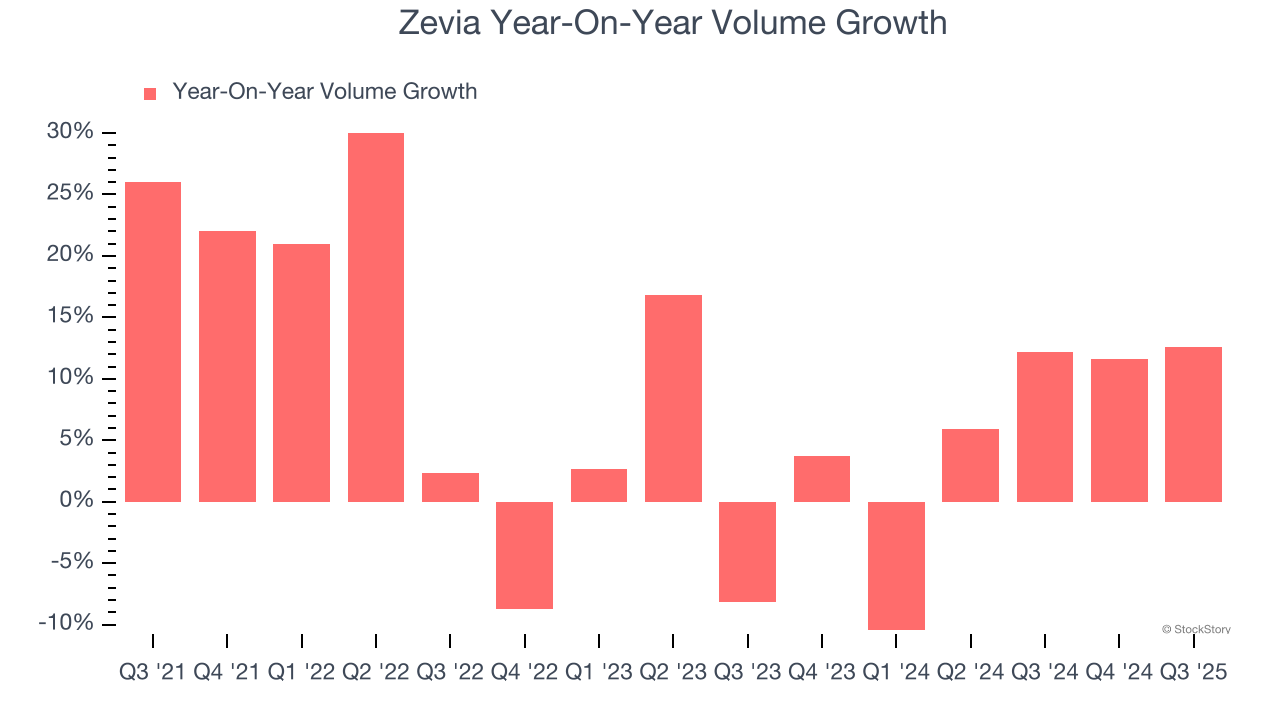

- Sales Volumes rose 12.6% year on year, in line with the same quarter last year

- Market Capitalization: $155.5 million

Company Overview

With a primary focus on soda but also a presence in energy drinks and teas, Zevia (NYSE:ZVIA) is a better-for-you beverage company.

Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years.

With $162.8 million in revenue over the past 12 months, Zevia is a small consumer staples company, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with retailers.

As you can see below, Zevia struggled to increase demand as its $162.8 million of sales for the trailing 12 months was close to its revenue three years ago. To its credit, however, consumers bought more of its products - we’ll explore what this means in the "Volume Growth" section.

This quarter, Zevia reported year-on-year revenue growth of 12.3%, and its $40.84 million of revenue exceeded Wall Street’s estimates by 3.7%. Company management is currently guiding for a 1.4% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 4.2% over the next 12 months. While this projection indicates its newer products will catalyze better top-line performance, it is still below the sector average.

Microsoft, Alphabet, Coca-Cola, Monster Beverage—all began as under-the-radar growth stories riding a massive trend. We’ve identified the next one: a profitable AI semiconductor play Wall Street is still overlooking. Go here for access to our full report.

Volume Growth

Revenue growth can be broken down into changes in price and volume (the number of units sold). While both are important, volume is the lifeblood of a successful staples business as there’s a ceiling to what consumers will pay for everyday goods; they can always trade down to non-branded products if the branded versions are too expensive.

Zevia’s average quarterly volume growth was a robust 5.9% over the last two years. This is good because meaningful volume growth is hard to come by in the stable consumer staples sector.

In Zevia’s Q3 2025, sales volumes jumped 12.6% year on year. This result was an acceleration from its historical levels, certainly a positive signal.

Key Takeaways from Zevia’s Q3 Results

We were impressed by Zevia’s optimistic EBITDA guidance for next quarter, which blew past analysts’ expectations. We were also excited its EBITDA outperformed Wall Street’s estimates by a wide margin. On the other hand, its gross margin missed. Zooming out, we think this quarter featured some important positives. The stock traded up 11% to $2.62 immediately after reporting.

Zevia put up rock-solid earnings, but one quarter doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.