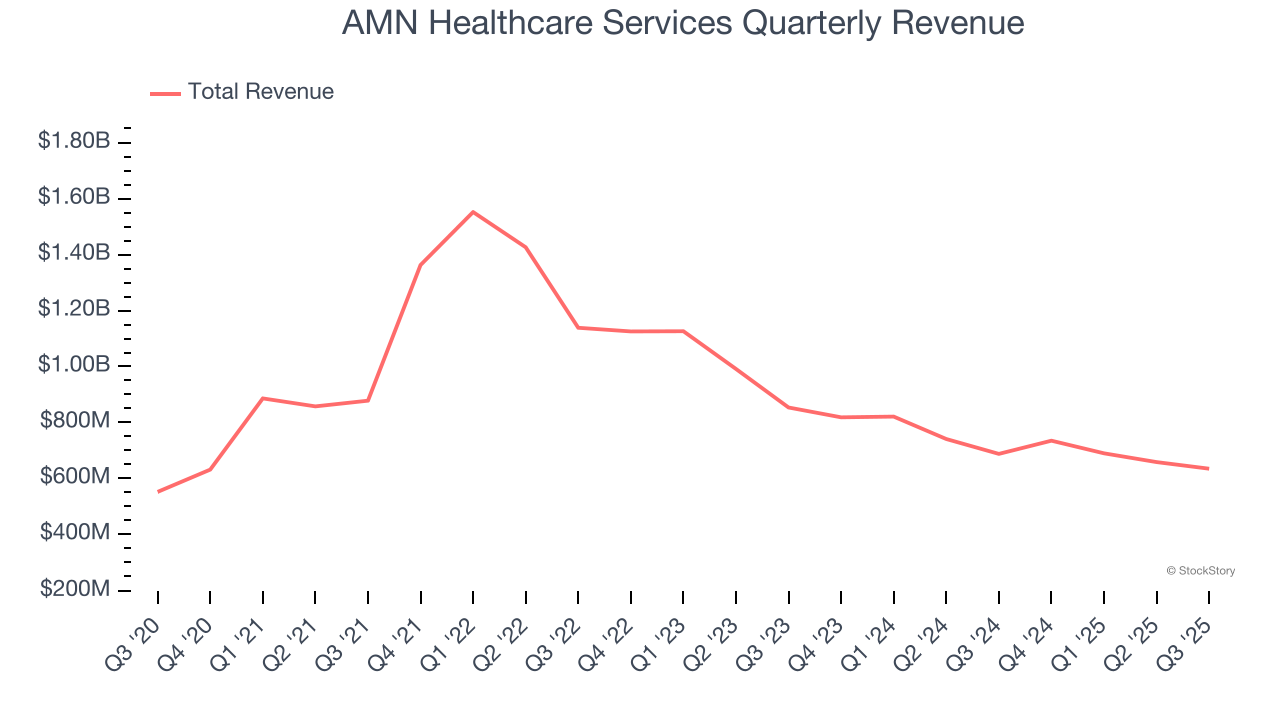

Healthcare staffing company AMN Healthcare Services (NYSE:AMN) reported revenue ahead of Wall Streets expectations in Q3 CY2025, but sales fell by 7.7% year on year to $634.5 million. On top of that, next quarter’s revenue guidance ($722.5 million at the midpoint) was surprisingly good and 16.4% above what analysts were expecting. Its non-GAAP profit of $0.39 per share was 95.2% above analysts’ consensus estimates.

Is now the time to buy AMN Healthcare Services? Find out by accessing our full research report, it’s free for active Edge members.

AMN Healthcare Services (AMN) Q3 CY2025 Highlights:

- Revenue: $634.5 million vs analyst estimates of $618 million (7.7% year-on-year decline, 2.7% beat)

- Adjusted EPS: $0.39 vs analyst estimates of $0.20 (95.2% beat)

- Adjusted EBITDA: $57.51 million vs analyst estimates of $48.86 million (9.1% margin, 17.7% beat)

- Revenue Guidance for Q4 CY2025 is $722.5 million at the midpoint, above analyst estimates of $620.6 million

- Operating Margin: 7.5%, up from 3.2% in the same quarter last year

- Free Cash Flow Margin: 3.6%, down from 6.9% in the same quarter last year

- Sales Volumes fell 10.6% year on year (-23.5% in the same quarter last year)

- Market Capitalization: $790.6 million

“The AMN team responded impressively to the second quarter's marketplace uncertainty, delivering third quarter revenue and earnings ahead of our guidance,” said Cary Grace, President and Chief Executive Officer of AMN Healthcare.

Company Overview

With a network of thousands of healthcare professionals ranging from nurses to physicians to executives, AMN Healthcare (NYSE:AMN) provides healthcare workforce solutions including temporary staffing, permanent placement, and technology platforms for hospitals and healthcare facilities across the United States.

Revenue Growth

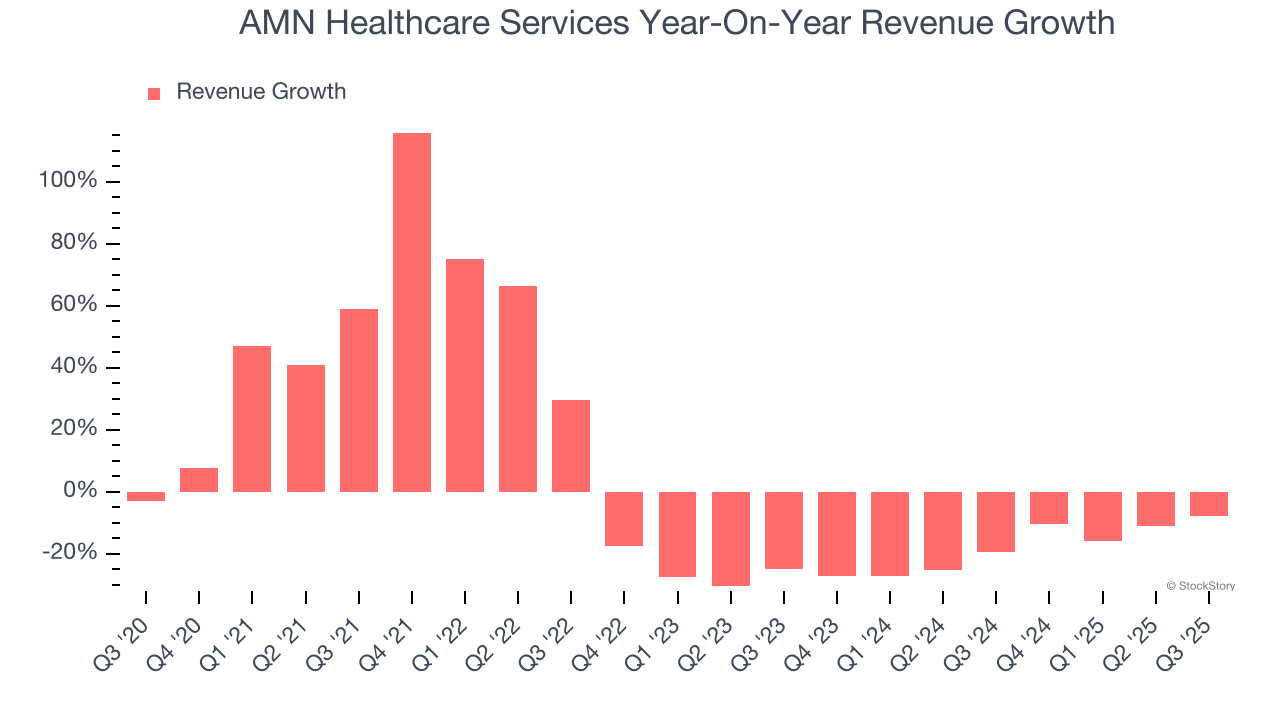

Examining a company’s long-term performance can provide clues about its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Regrettably, AMN Healthcare Services’s sales grew at a tepid 2.9% compounded annual growth rate over the last five years. This was below our standards and is a tough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within healthcare, a half-decade historical view may miss recent innovations or disruptive industry trends. AMN Healthcare Services’s performance shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 18.6% annually.

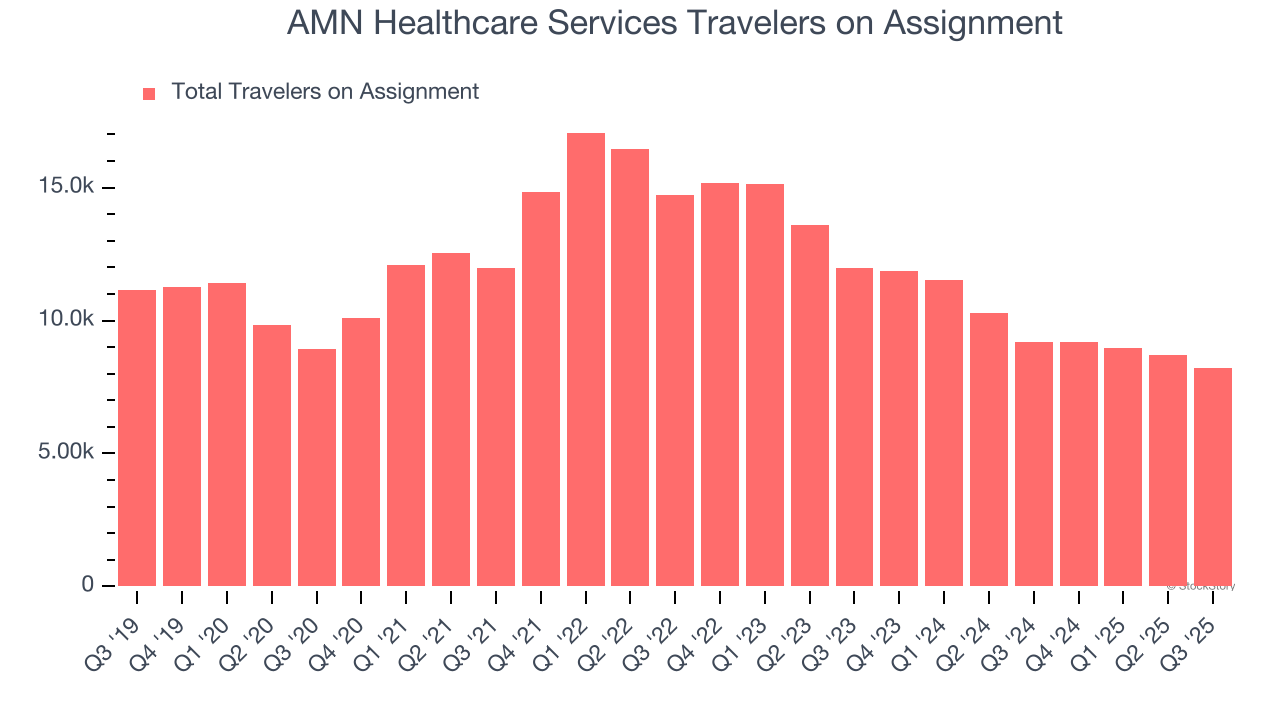

AMN Healthcare Services also reports its number of travelers on assignment, which reached 8,203 in the latest quarter. Over the last two years, AMN Healthcare Services’s travelers on assignment averaged 20.5% year-on-year declines. Because this number is lower than its revenue growth, we can see the company benefited from price increases.

This quarter, AMN Healthcare Services’s revenue fell by 7.7% year on year to $634.5 million but beat Wall Street’s estimates by 2.7%. Company management is currently guiding for a 1.7% year-on-year decline in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to decline by 7.3% over the next 12 months. Although this projection is better than its two-year trend, it’s hard to get excited about a company that is struggling with demand.

Microsoft, Alphabet, Coca-Cola, Monster Beverage—all began as under-the-radar growth stories riding a massive trend. We’ve identified the next one: a profitable AI semiconductor play Wall Street is still overlooking. Go here for access to our full report.

Operating Margin

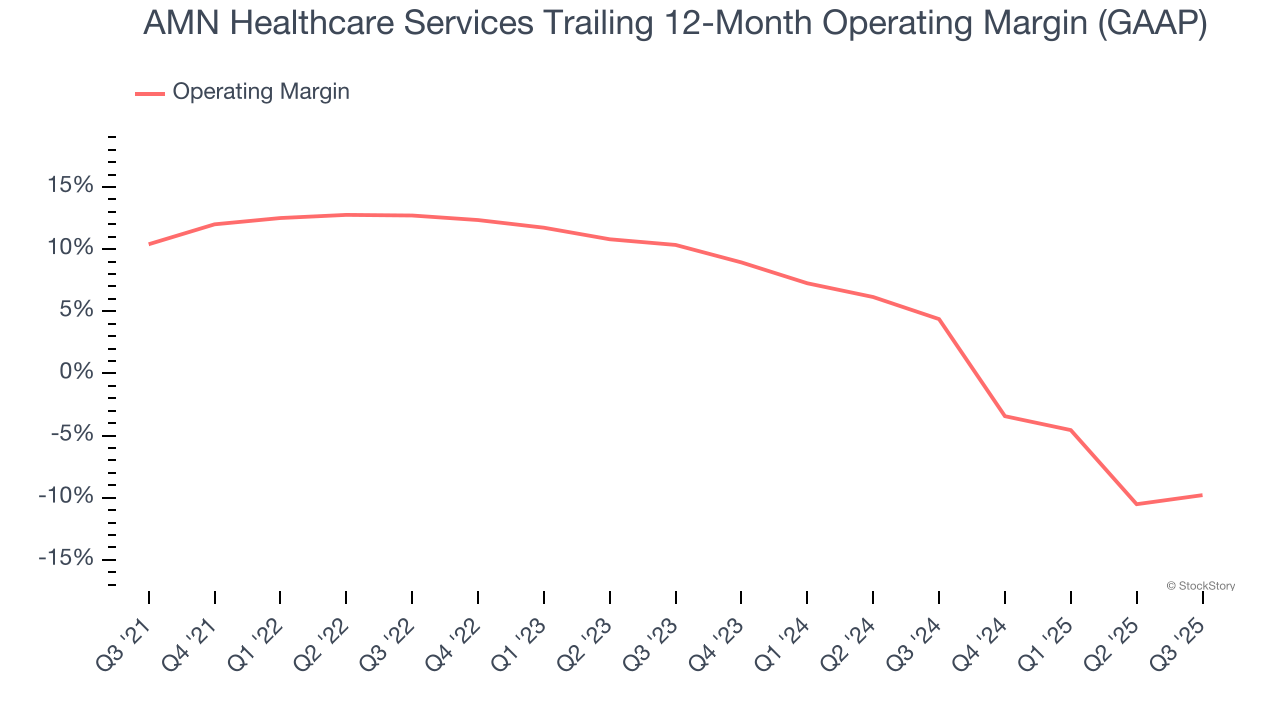

AMN Healthcare Services was profitable over the last five years but held back by its large cost base. Its average operating margin of 7.1% was weak for a healthcare business.

Looking at the trend in its profitability, AMN Healthcare Services’s operating margin decreased by 20.2 percentage points over the last five years. The company’s two-year trajectory also shows it failed to get its profitability back to the peak as its margin fell by 20.1 percentage points. This performance was poor no matter how you look at it - it shows its expenses were rising and it couldn’t pass those costs onto its customers.

This quarter, AMN Healthcare Services generated an operating margin profit margin of 7.5%, up 4.3 percentage points year on year. This increase was a welcome development, especially since its revenue fell, showing it was more efficient because it scaled down its expenses.

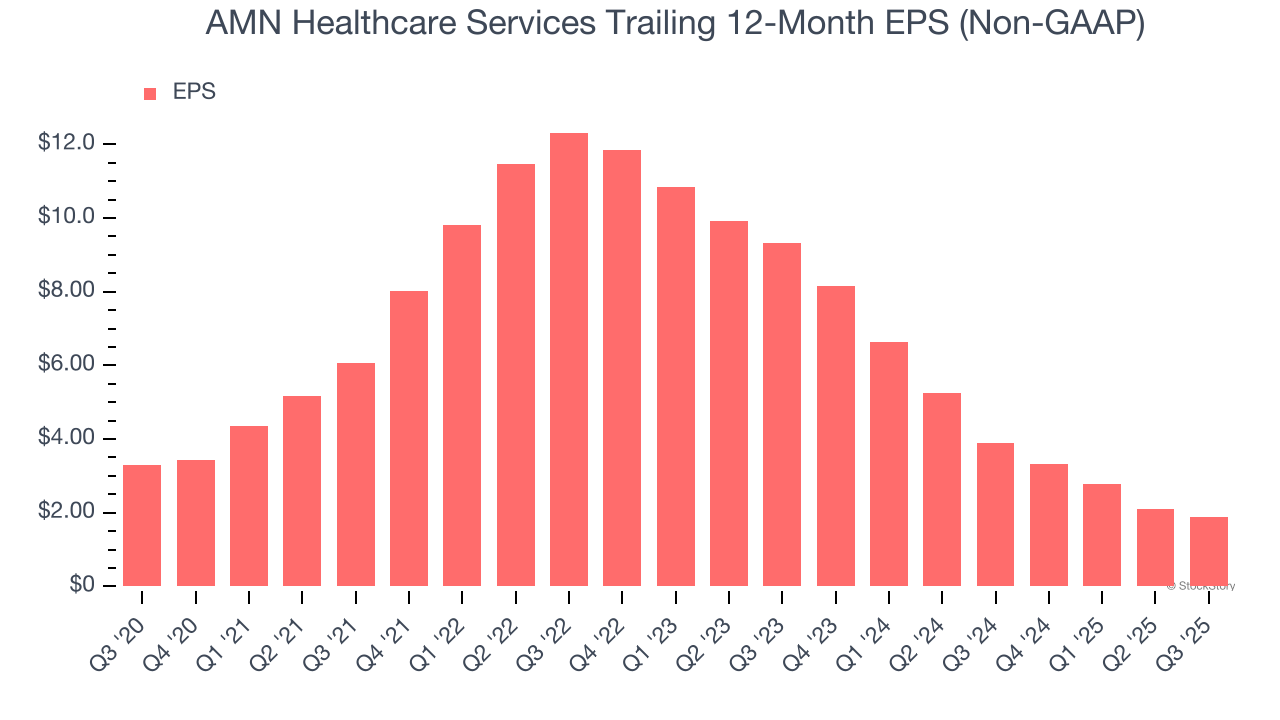

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sadly for AMN Healthcare Services, its EPS declined by 10.5% annually over the last five years while its revenue grew by 2.9%. This tells us the company became less profitable on a per-share basis as it expanded due to non-fundamental factors such as interest expenses and taxes.

Diving into the nuances of AMN Healthcare Services’s earnings can give us a better understanding of its performance. As we mentioned earlier, AMN Healthcare Services’s operating margin expanded this quarter but declined by 20.2 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its lower earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q3, AMN Healthcare Services reported adjusted EPS of $0.39, down from $0.61 in the same quarter last year. Despite falling year on year, this print easily cleared analysts’ estimates. Over the next 12 months, Wall Street expects AMN Healthcare Services’s full-year EPS of $1.89 to shrink by 49.7%.

Key Takeaways from AMN Healthcare Services’s Q3 Results

It was good to see AMN Healthcare Services beat analysts’ EPS expectations this quarter. We were also glad its revenue guidance for next quarter trumped Wall Street’s estimates. Zooming out, we think this was a solid print. The stock traded up 5.3% to $19.40 immediately after reporting.

AMN Healthcare Services put up rock-solid earnings, but one quarter doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.