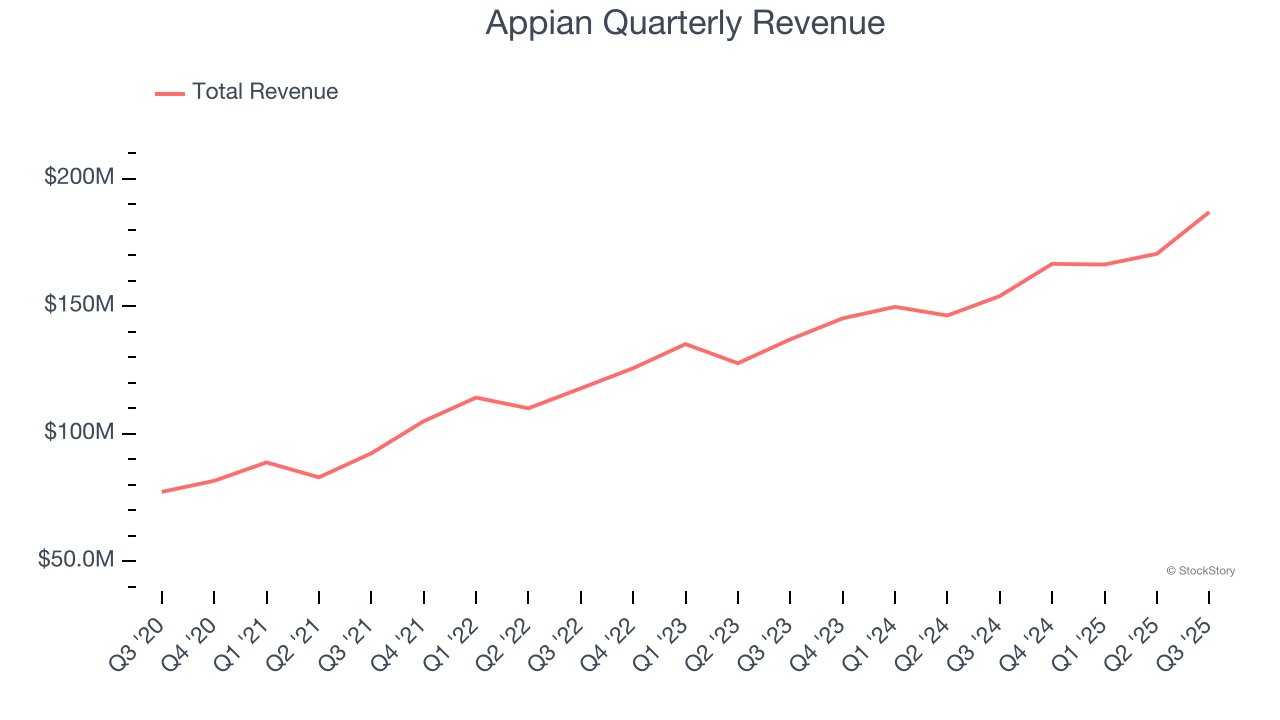

Low-code automation software company Appian (NASDAQ:APPN) beat Wall Street’s revenue expectations in Q3 CY2025, with sales up 21.4% year on year to $187 million. Guidance for next quarter’s revenue was better than expected at $189 million at the midpoint, 0.9% above analysts’ estimates. Its non-GAAP profit of $0.32 per share was significantly above analysts’ consensus estimates.

Is now the time to buy Appian? Find out by accessing our full research report, it’s free for active Edge members.

Appian (APPN) Q3 CY2025 Highlights:

- Revenue: $187 million vs analyst estimates of $174.1 million (21.4% year-on-year growth, 7.4% beat)

- Adjusted EPS: $0.32 vs analyst estimates of $0.05 (significant beat)

- Adjusted Operating Income: $29.76 billion vs analyst estimates of $7.90 million (15,915% margin, significant beat)

- Revenue Guidance for Q4 CY2025 is $189 million at the midpoint, above analyst estimates of $187.4 million

- Management raised its full-year Adjusted EPS guidance to $0.52 at the midpoint, a 62.5% increase

- EBITDA guidance for the full year is $68.5 million at the midpoint, above analyst estimates of $52.73 million

- Operating Margin: 7%, up from -4.6% in the same quarter last year

- Free Cash Flow was $18.06 million, up from -$3.09 million in the previous quarter

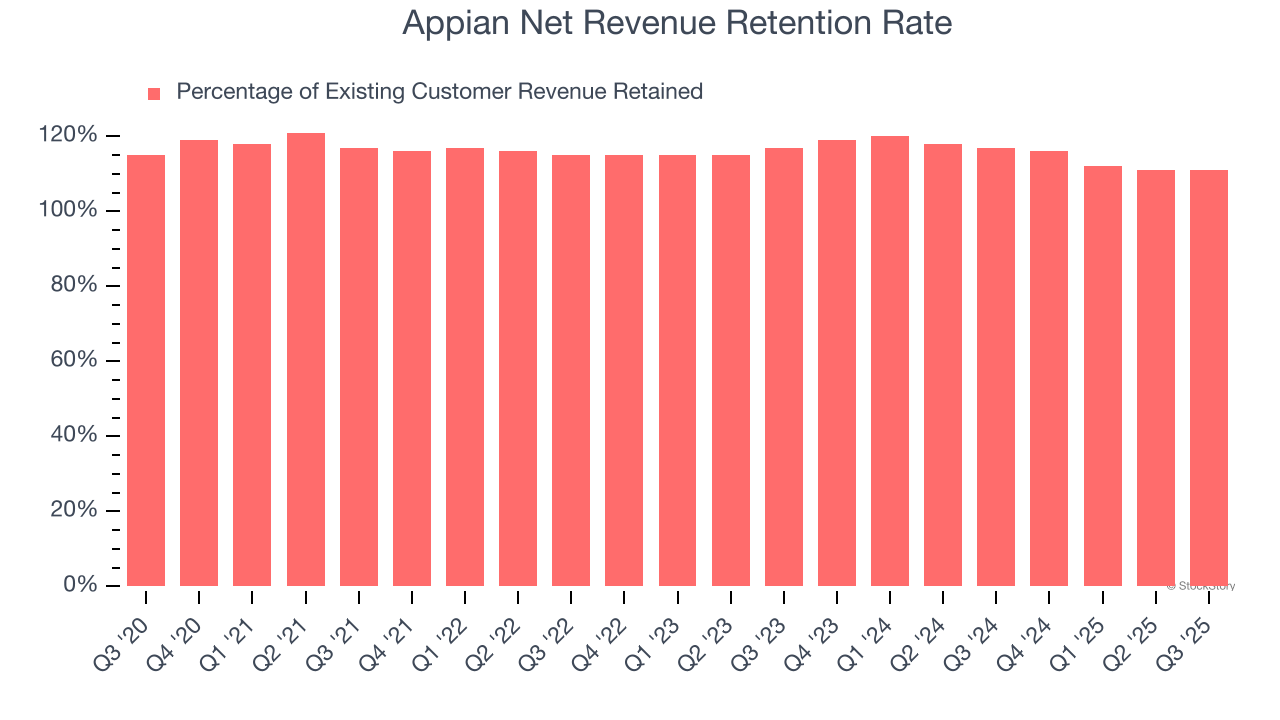

- Net Revenue Retention Rate: 111%, in line with the previous quarter

- Market Capitalization: $2.17 billion

Company Overview

Powering billions of transactions daily since its founding in 1999, Appian (NASDAQ:APPN) provides a low-code platform that helps businesses automate complex processes and operationalize artificial intelligence without extensive programming knowledge.

Revenue Growth

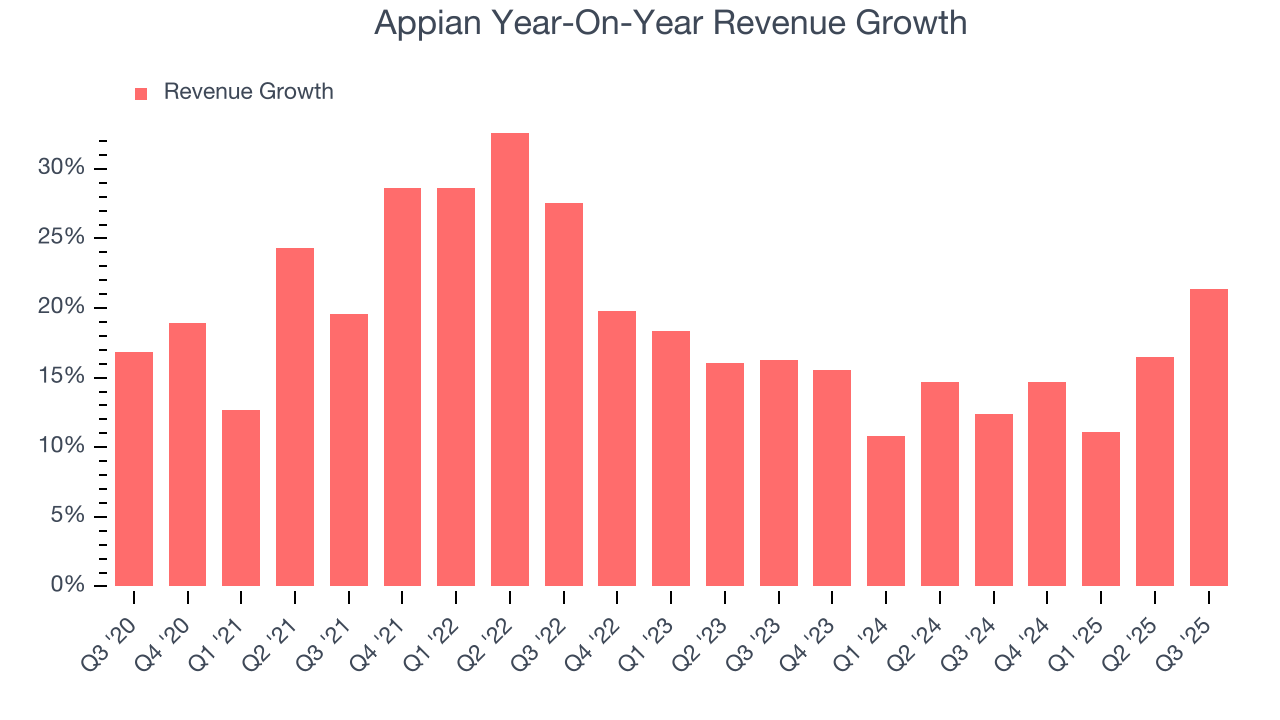

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last five years, Appian grew its sales at a decent 18.8% compounded annual growth rate. Its growth was slightly above the average software company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within software, a half-decade historical view may miss recent innovations or disruptive industry trends. Appian’s recent performance shows its demand has slowed as its annualized revenue growth of 14.6% over the last two years was below its five-year trend.

This quarter, Appian reported robust year-on-year revenue growth of 21.4%, and its $187 million of revenue topped Wall Street estimates by 7.4%. Company management is currently guiding for a 13.4% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 9% over the next 12 months, a deceleration versus the last two years. This projection is underwhelming and suggests its products and services will face some demand challenges.

While Wall Street chases Nvidia at all-time highs, an under-the-radar semiconductor supplier is dominating a critical AI component these giants can’t build without. Click here to access our free report one of our favorites growth stories.

Customer Retention

One of the best parts about the software-as-a-service business model (and a reason why they trade at high valuation multiples) is that customers typically spend more on a company’s products and services over time.

Appian’s net revenue retention rate, a key performance metric measuring how much money existing customers from a year ago are spending today, was 113% in Q3. This means Appian would’ve grown its revenue by 12.5% even if it didn’t win any new customers over the last 12 months.

Despite falling over the last year, Appian still has a good net retention rate, proving that customers are satisfied with its software and getting more value from it over time, which is always great to see.

Key Takeaways from Appian’s Q3 Results

We were impressed by how significantly Appian blew past analysts’ EBITDA expectations this quarter. We were also glad its full-year EBITDA guidance trumped Wall Street’s estimates. On the other hand, its EBITDA guidance for next quarter missed. Overall, we think this was still a solid quarter with some key areas of upside. The stock traded up 10.8% to $32.50 immediately following the results.

Appian had an encouraging quarter, but one earnings result doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.