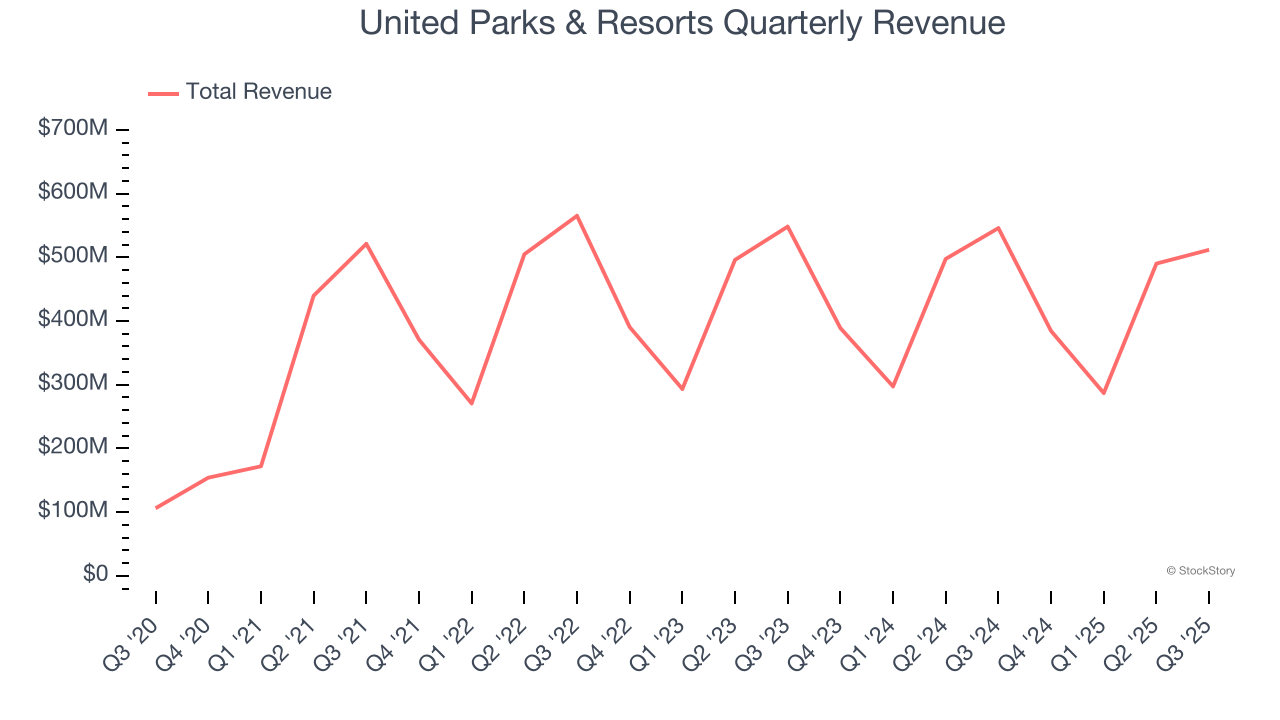

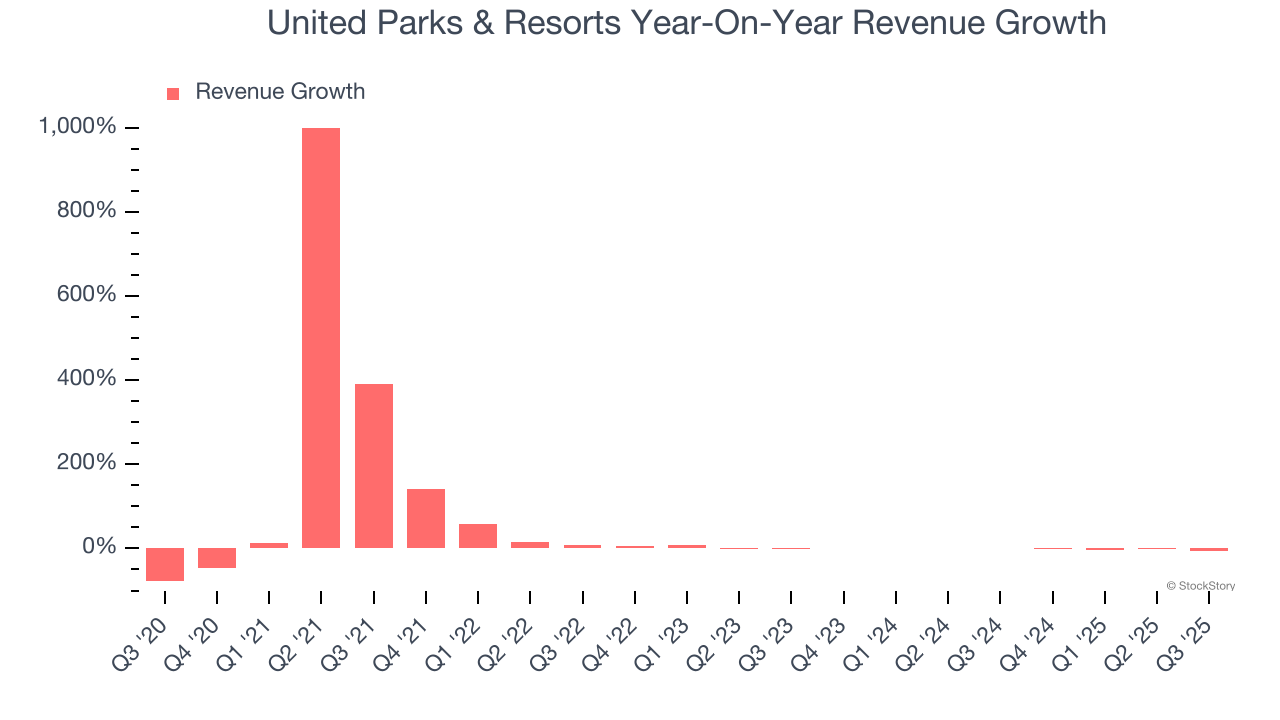

Theme park operator United Parks & Resorts (NYSE:PRKS) fell short of the markets revenue expectations in Q3 CY2025, with sales falling 6.2% year on year to $511.9 million. Its GAAP profit of $1.61 per share was 28.8% below analysts’ consensus estimates.

Is now the time to buy United Parks & Resorts? Find out by accessing our full research report, it’s free for active Edge members.

United Parks & Resorts (PRKS) Q3 CY2025 Highlights:

- Revenue: $511.9 million vs analyst estimates of $539.8 million (6.2% year-on-year decline, 5.2% miss)

- EPS (GAAP): $1.61 vs analyst expectations of $2.26 (28.8% miss)

- Adjusted EBITDA: $216.3 million vs analyst estimates of $252.1 million (42.3% margin, 14.2% miss)

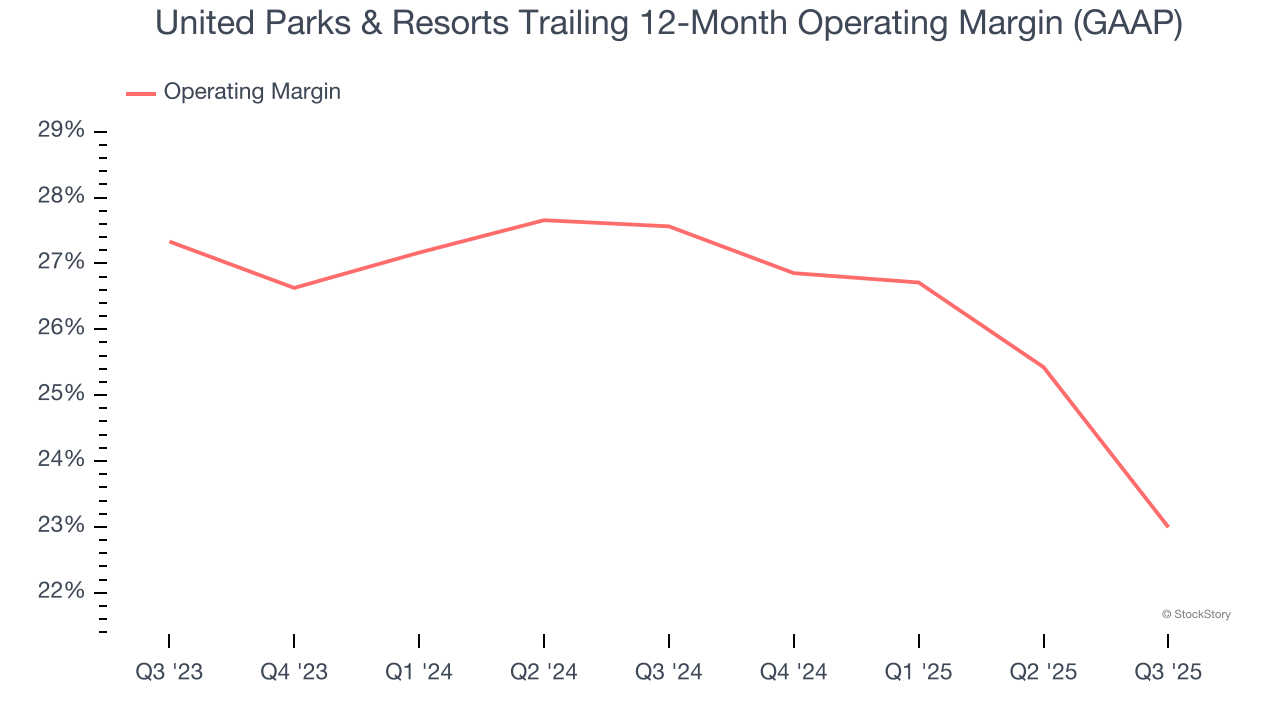

- Operating Margin: 29.6%, down from 36.8% in the same quarter last year

- Free Cash Flow Margin: 7.4%, down from 12.4% in the same quarter last year

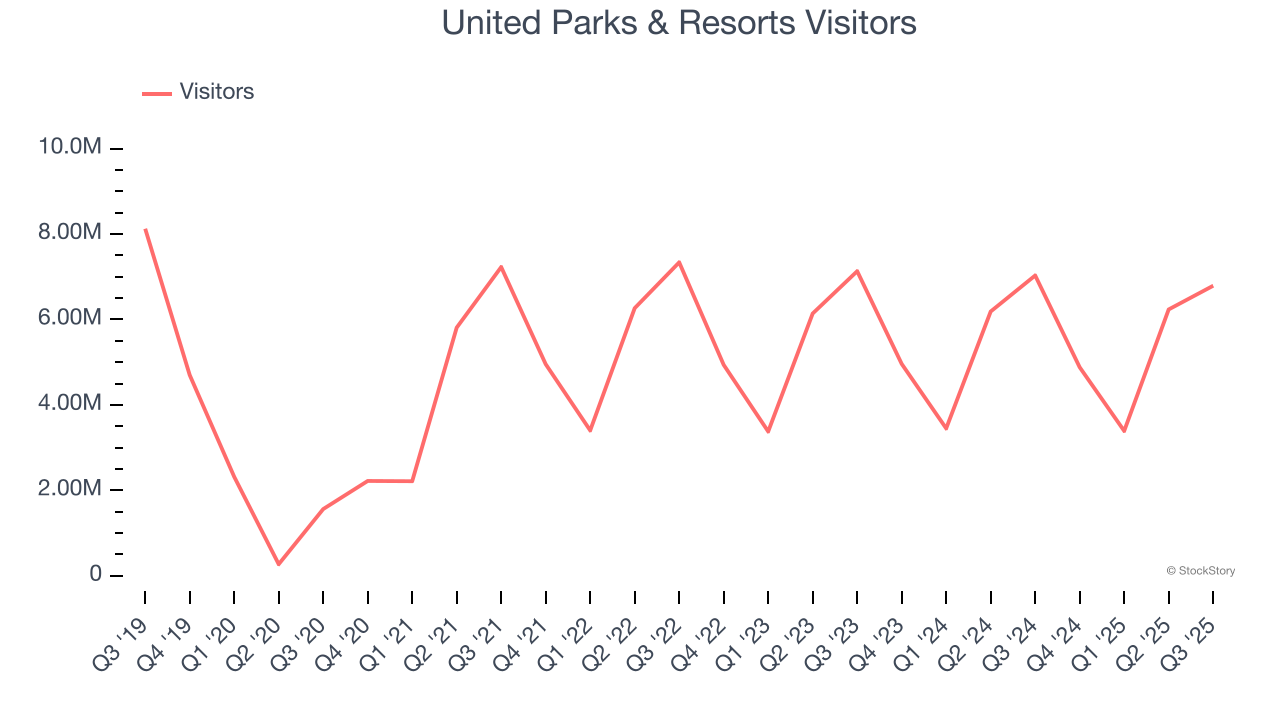

- Visitors: 6.79 million, down 240,000 year on year

- Market Capitalization: $2.54 billion

"We are obviously not happy with the results we delivered in the quarter. Performance during the quarter was negatively impacted by an unfavorable calendar shift, poor weather during peak holiday periods, a decline in international visitation and less than optimal execution. The consumer environment in the U.S. appears to be inconsistent, as has been outlined by a number of other leisure and hospitality businesses. Nonetheless, we can and expect to do better," said Marc Swanson, Chief Executive Officer of United Parks & Resorts Inc.

Company Overview

Parent company of SeaWorld and home of the world-famous Shamu, United Parks & Resorts (NYSE:PRKS) is a theme park chain featuring marine life, live entertainment, roller coasters, and waterparks.

Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Luckily, United Parks & Resorts’s sales grew at an impressive 23.8% compounded annual growth rate over the last five years. Its growth beat the average consumer discretionary company and shows its offerings resonate with customers, a helpful starting point for our analysis.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. United Parks & Resorts’s recent performance marks a sharp pivot from its five-year trend as its revenue has shown annualized declines of 1.6% over the last two years. Note that COVID hurt United Parks & Resorts’s business in 2020 and part of 2021, and it bounced back in a big way thereafter.

We can dig further into the company’s revenue dynamics by analyzing its number of visitors, which reached 6.79 million in the latest quarter. Over the last two years, United Parks & Resorts’s visitors were flat. Because this number aligns with its revenue growth during the same period, we can see the company’s monetization was fairly consistent.

This quarter, United Parks & Resorts missed Wall Street’s estimates and reported a rather uninspiring 6.2% year-on-year revenue decline, generating $511.9 million of revenue.

Looking ahead, sell-side analysts expect revenue to grow 4.4% over the next 12 months. While this projection implies its newer products and services will catalyze better top-line performance, it is still below the sector average. At least the company is tracking well in other measures of financial health.

The 1999 book Gorilla Game predicted Microsoft and Apple would dominate tech before it happened. Its thesis? Identify the platform winners early. Today, enterprise software companies embedding generative AI are becoming the new gorillas. a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

United Parks & Resorts’s operating margin has shrunk over the last 12 months, but it still averaged 25.3% over the last two years, elite for a consumer discretionary business. This shows it’s an well-run company with an efficient cost structure, and its top-notch historical revenue growth also suggests its margin dropped because it ramped up investments to capture market share, a strategy that seems to have paid off so far.

This quarter, United Parks & Resorts generated an operating margin profit margin of 29.6%, down 7.2 percentage points year on year. This contraction shows it was less efficient because its expenses increased relative to its revenue.

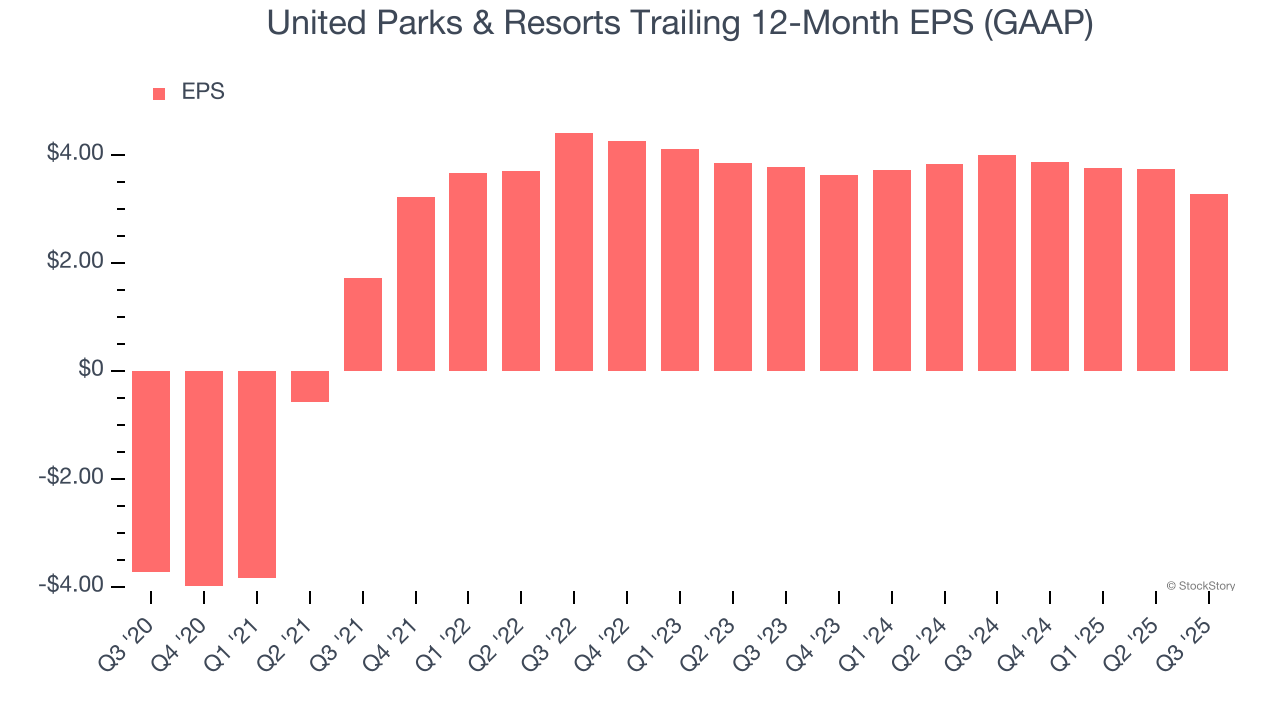

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

United Parks & Resorts’s full-year EPS flipped from negative to positive over the last five years. This is a good sign and shows it’s at an inflection point.

In Q3, United Parks & Resorts reported EPS of $1.61, down from $2.08 in the same quarter last year. This print missed analysts’ estimates, but we care more about long-term EPS growth than short-term movements. Over the next 12 months, Wall Street expects United Parks & Resorts’s full-year EPS of $3.27 to grow 47.5%.

Key Takeaways from United Parks & Resorts’s Q3 Results

We struggled to find many positives in these results. Its number of visitors missed and its revenue fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 5.9% to $43.50 immediately following the results.

United Parks & Resorts’s latest earnings report disappointed. One quarter doesn’t define a company’s quality, so let’s explore whether the stock is a buy at the current price. When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.