McDonald's currently trades at $316.29 per share and has shown little upside over the past six months, posting a middling return of 4.1%. However, the stock is beating the S&P 500’s 7% decline during that period.

Given the relative strength, is there still a buying opportunity in MCD? Or is the market overestimating its value? Find out in our full research report, it’s free.

Why Does MCD Stock Spark Debate?

With nicknames spanning Mickey D's in the U.S. to Makku in Japan, McDonald’s (NYSE:MCD) is a fast-food behemoth known for its convenience and broken ice cream machines.

Two Positive Attributes:

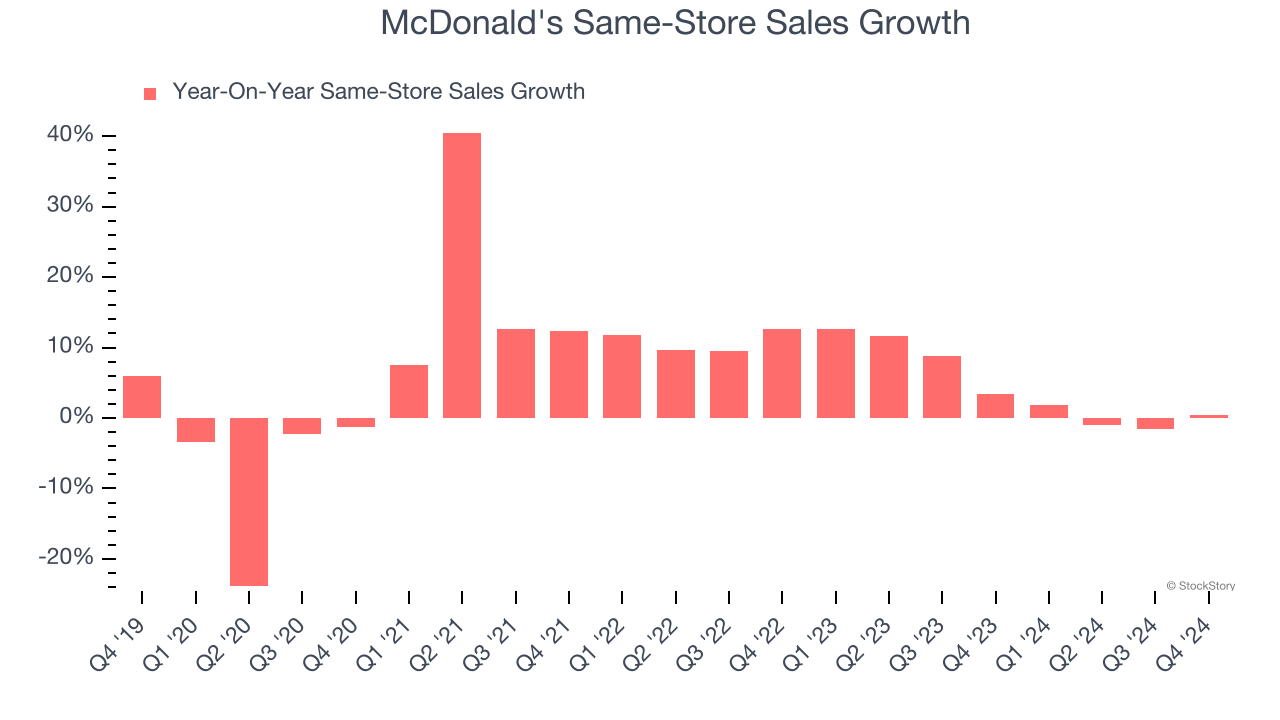

1. Surging Same-Store Sales Show Increasing Demand

Same-store sales is a key performance indicator used to measure organic growth at restaurants open for at least a year.

McDonald's has been one of the most successful restaurant chains over the last two years thanks to skyrocketing demand within its existing dining locations. On average, the company has posted exceptional year-on-year same-store sales growth of 4.5%.

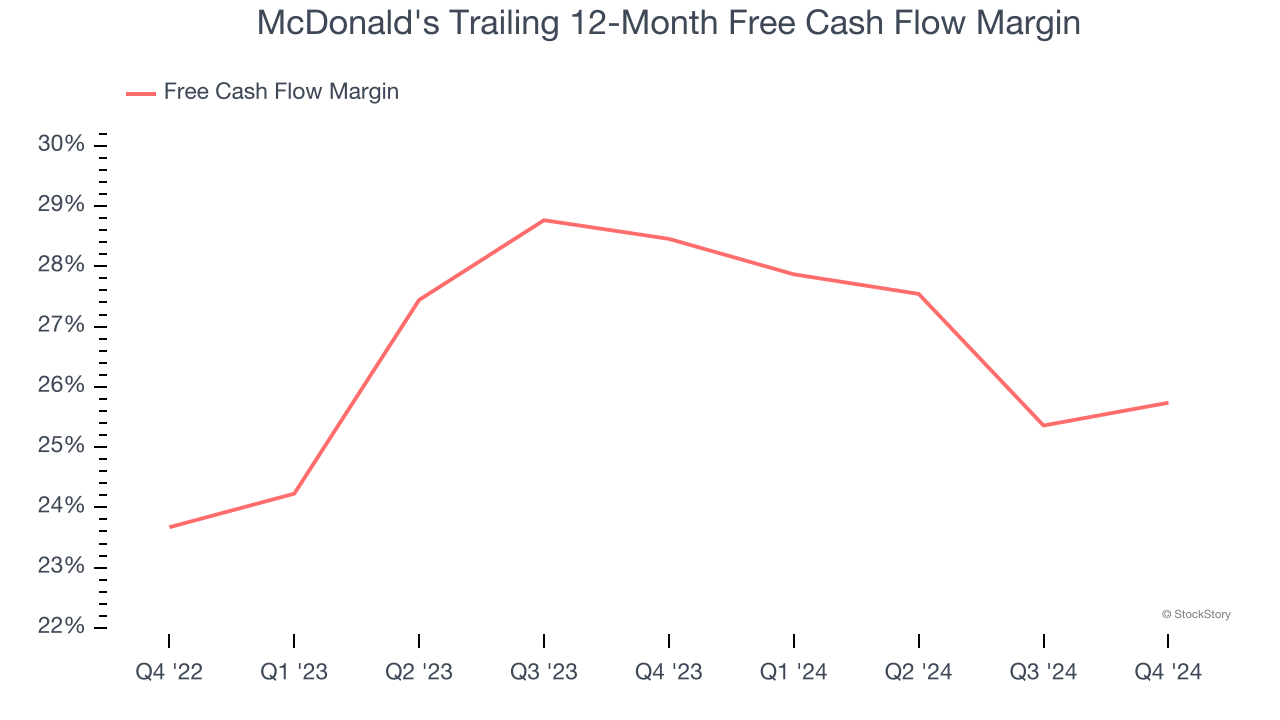

2. Excellent Free Cash Flow Margin Boosts Reinvestment Potential

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

McDonald's has shown terrific cash profitability, driven by its lucrative business model that enables it to reinvest, return capital to investors, and stay ahead of the competition. The company’s free cash flow margin was among the best in the restaurant sector, averaging 27.1% over the last two years.

One Reason to be Careful:

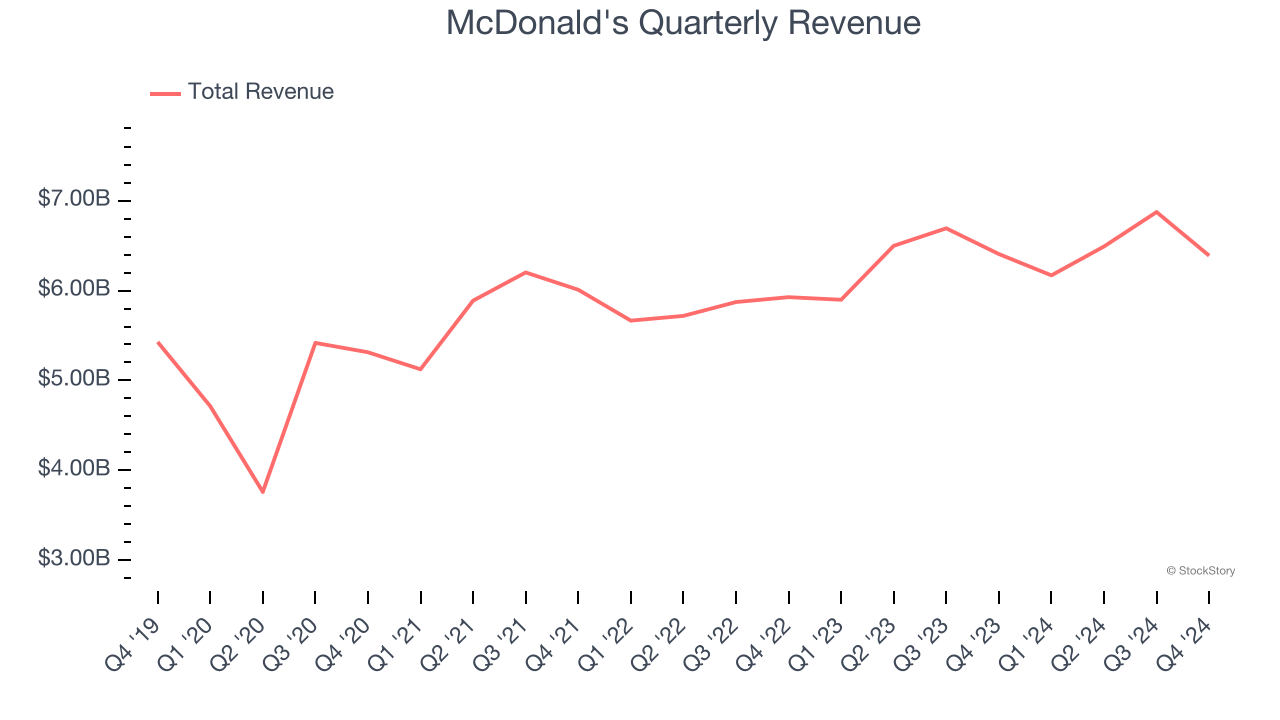

Long-Term Revenue Growth Disappoints

A company’s long-term sales performance is one signal of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Over the last five years, McDonald's grew its sales at a sluggish 3.9% compounded annual growth rate. This wasn’t a great result compared to the rest of the restaurant sector, but there are still things to like about McDonald's.

Final Judgment

McDonald’s positive characteristics outweigh the negatives, and after its recent outperformance in a weaker market environment, the stock trades at 25.6× forward price-to-earnings (or $316.29 per share). Is now the time to initiate a position? See for yourself in our in-depth research report, it’s free.

Stocks We Like Even More Than McDonald's

The market surged in 2024 and reached record highs after Donald Trump’s presidential victory in November, but questions about new economic policies are adding much uncertainty for 2025.

While the crowd speculates what might happen next, we’re homing in on the companies that can succeed regardless of the political or macroeconomic environment. Put yourself in the driver’s seat and build a durable portfolio by checking out our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Sterling Infrastructure (+1,096% five-year return). Find your next big winner with StockStory today for free.